A Tool That Pulls You Out of The Worst Situation

I paid off over $50,000 in debt in 19 months! And I'll show you exactly step-by-step how I did it!

Hello!

My name is Kuba, I'm 34 years old, and just 3 years ago I was the typical guy who didn’t care about finances. I lived paycheck to paycheck, but I never had enough to last until the end of the month—within the first two days, almost my entire paycheck disappeared on silly things. I spent money on everything: a new iPhone for $1,200 because "I need the latest model to impress my friends," several pairs of shoes for $400 each because "I need options," a vacation to Bali on installments for $4,000, restaurants, clubs, and dinners with friends every weekend costing $300–500 per night, and impulsive online shopping for gadgets and clothes—about $800 a month without a second thought. Budget knowledge? None, because why bother? Laziness? I preferred scrolling through social media rather than checking my account. Extravagance? Absolutely: I bought things I couldn’t afford just to appear rich. I had short-lived enthusiasm for everything—for example, I started running, and after two weeks, I bought a $1,500 heart rate monitor watch, $200 sunglasses, and $400 shoes because "I’m a professional now, I can’t do it without these." Of course, I ran for two months and then lost interest—another "passion of a lifetime" for 3 months, quickly forgotten, while the loan for the watch and installments for the shoes haunted me for another year and a half. How foolish was that! And when I ran short, what did I do? I borrowed $200–500 from family and friends every month, saying, "Lend me some, I’ll pay you back." And when that wasn’t enough—I took out another payday loan. I created debts to cover debts—a spiral with no way out. Before I knew it, I had $50,000 in debt. Monthly, I was paying over $1,500 in installments, and life had become a nightmare, even though I’d been having a blast for a while. Eventually, I started denying the problem: stress, sleepless nights, avoiding money conversations. I thought it was "normal"—everyone lives like this, right?

The turning point hit me like a bolt from the blue.

It was a Friday evening—I was out with friends at a restaurant, and after dinner, we planned to go to a club. When I went to pay, the transaction was declined. My account was overdrawn, the bank denied the overdraft, and I stood there like an idiot in front of my friends, who looked at me with pity. "Don’t worry, I’ll cover it," a friend said, and I felt as if someone had slapped me in the face. I went home furious and humiliated, opened my banking app, and saw the balance—debts had devoured everything, and I’d hit rock bottom. This wasn’t "okay"—suddenly, I realized I was losing control of my life. I couldn’t sleep, thinking about the future: "What if I lose my job? How will I support a family? This isn’t living; it’s a trap!" The next morning, in desperation, I scoured the entire internet, typing "how to get out of debt fast." I found a forum where people with similar problems shared how they’d escaped this mess. Everyone kept repeating one thing: LunchMoney app! A coworker had once mentioned this expense-tracking app, so I clicked. I downloaded LunchMoney because it promised quick help and simplicity. The app integrates with banks, categorizes expenses, and shows where the money is disappearing—perfect for a novice like me. This was my game-changer—an app that doesn’t judge but helps bring order to chaos. I logged in, imported my data, and saw in black and white how my "little pleasures" had buried me in this mess. I realized things were really bad and stopped pretending I had control. I sat down in the kitchen with coffee and opened LunchMoney.

The two most important steps in my life:

Step 1

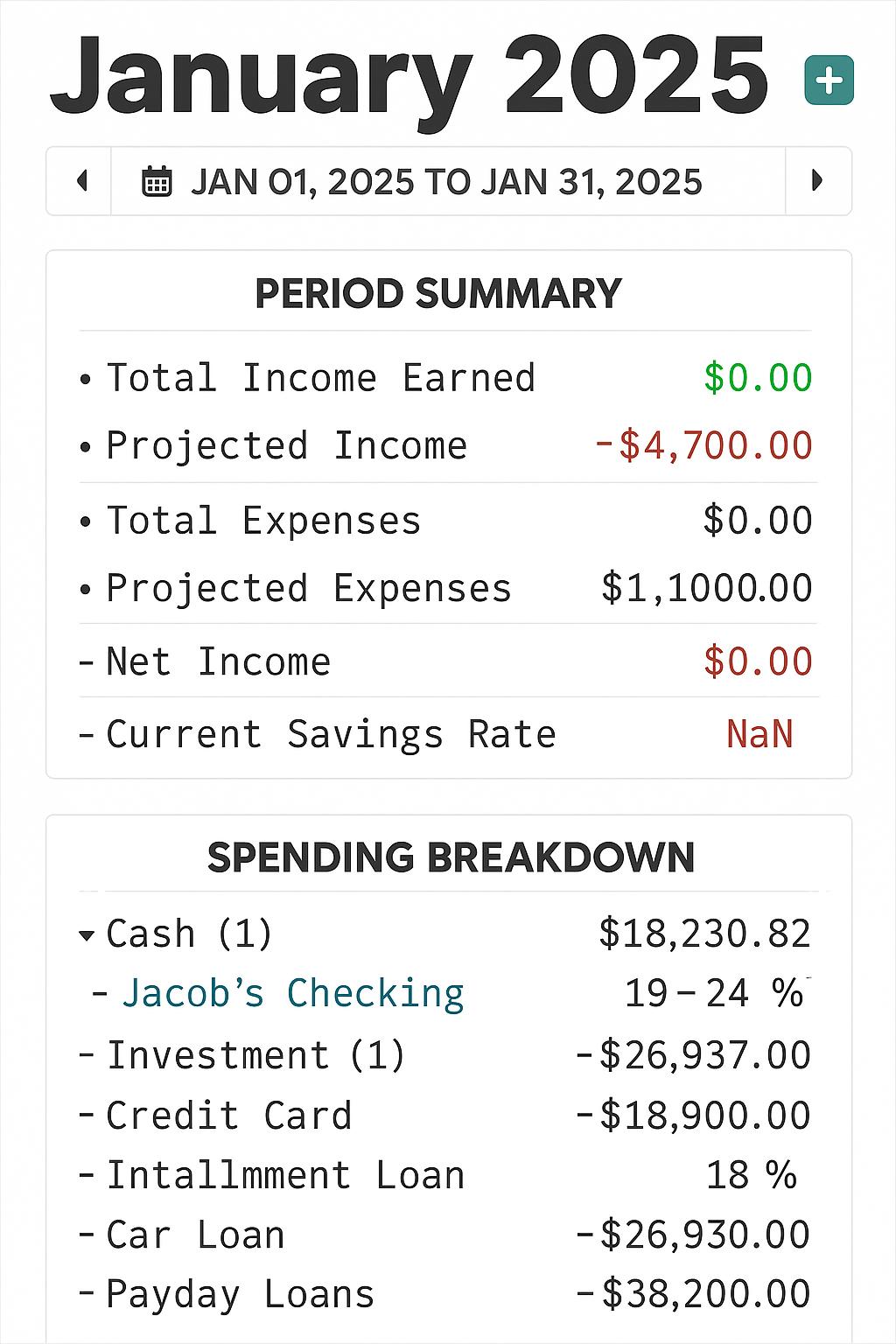

I imported transactions from all my accounts and cards. The app automatically showed me ALL my debts, broken down into categories:

- Revolut credit card – $20,000 (19% interest)

- Installment loan at Credit Agricole – $10,000 (18%)

- Auto loan – $15,000 (7.9%)

- Two payday loans – $5,000 (29% and 39%—brutal)

Total: $50,000. LunchMoney showed spending trends, like impulsive purchases: $800/month, and how much I was losing in interest—about $500/month. It automatically flagged transactions related to debts, and visual reports illustrated how extravagance (eating out, gadgets) fueled the spiral. It was like a cold shower—the app gave me a full picture of the chaos in 10 minutes.

Step 2

I consolidated my debts (the most important trick, and LunchMoney helped me figure it out). How did I come up with this? The app showed me that interest was eating up the most—reports revealed I was paying an average of 23% annually, meaning hundreds of dollars lost every month. This motivated me: "I have to lower the interest!" I went to the bank and said, "I want to combine everything into one loan with a lower interest rate." Instead of paying an average of 23% annually, I now pay just 8.9%. My monthly installment dropped from ~$1,500 to $1,100 → instantly $400 more in my pocket. What did this give me? Savings on interest, less stress from multiple payments, and motivation to pay off faster—the app tracked this as "budget goals," showing real-time progress.

LunchMoney tracked my progress:

When I paid off the first Revolut card ($20,000), the app showed the snowball effect—the freed-up installment (about $350) was automatically added to the next loan payment. I received a notification: "Congratulations, you’ve paid off a debt! You’re amazing! Free funds redirected to the next goal in the 'Repayment' category," and the net worth tracker visualized the progress (from negatives to zero). Reports analyzed trends, suggesting further cuts—this motivated me as I watched debts shrink one after another! And finally, I did it! I paid everything off! I was a free, happy, and proud person! But that’s not all.

Thanks to LunchMoney, I not only got out of debt, but riding the wave of success and with an optimized plan, I managed to save a lot of money and build a financial safety net. After paying off all my debts, I now had a lot of money left over, which I decided to save—I now have tens of thousands of dollars that I can do whatever I want with, but I definitely won’t spend it on foolish things.

My honest recommendation in the end

LunchMoney isn’t another "magic" app.

It’s simply the best budgeting and expense-tracking tool I’ve ever tested (and I’ve tested them all: YNAB, Mint, Wallet, Spendee…).

If you:

- Have even one installment or payday loan

- Don’t know where your money is disappearing

- Want to finally feel in control

- Or simply want to start saving because you don’t have debts but don’t know how

…then click below and try LunchMoney free for 14 days

→ Click here to start for free (14-day trial)

https://lunchmoney.app?fp_ref=pmn&fp_sid=article2

Zero risk. If you don’t like it—simply uninstall.

But if you’re even 10% in the situation I was in—this could be the best click of your life.

Let me know in the comments how much debt you have—I’d be happy to help you get started.

I’m rooting for you!

Kuba

(Former debtor, now financially free)

*All stories and amounts in the article are based on my personal experiences.

The content published on this blog is for informational and educational purposes only. Investments in securities and other financial instruments always involve the risk of loss of your capital. The forecast or past performance is no guarantee of future results. It is essential to do your own analysis before making any investment. You can find the full version of the disclaimer here.